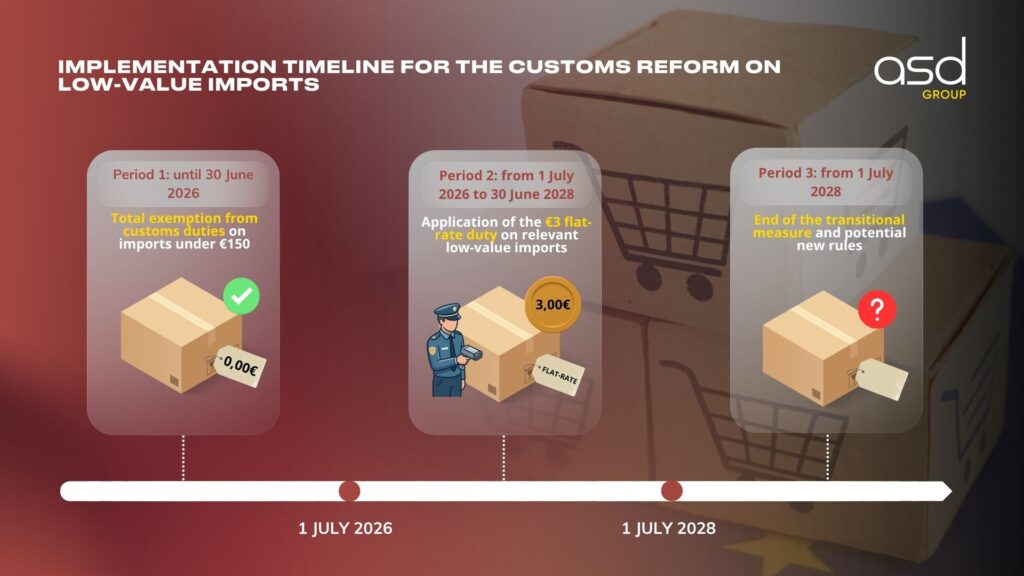

International e-commerce has undergone a major transformation since 1 July 2026. The entry into force of Regulation (EU) 2026/38211 establishes a new tax rule: the application of a flat-rate customs duty of €3 on low-value imports2. This measure, which will run until July 2028, profoundly changes the obligations of online sellers operating outside the European Union.

How does this reform work and how should companies adapt their logistics and customs compliance? Detailed analysis.

A new €3 customs duty from 1 July 2026

From 1 July 2026, the import procedures for low-value goods are permanently changed within the European Union. The flagship measure of this new regulation is the introduction of a flat-rate customs duty of €3. This duty applies to any goods whose intrinsic value is €150 or less upon entry into the customs territory of the Union.

It is crucial to note that this provision, provided for by Regulation (EU) 2026/3821, ends a long period of customs exemption from which low-value parcels traditionally benefited. The removal of this tax exemption is the cornerstone of a new era for international e-commerce. For businesses, this means that every shipment, regardless of its size (as long as it respects the €150 threshold), is now subject to this flat-rate cost, thereby modifying the cost structure of products sold remotely.

Why is the EU removing the exemption for parcels under €150?

The removal of the customs duty exemption for products under €150 is not an isolated measure. It is part of a much broader project: the reform of the Union Customs Code. The European Commission has identified several loopholes in the previous system, justifying this regulatory intervention.

The main objectives are fourfold:

| Objective | Justification |

| Modernisation | Adapt procedures to the explosion of global e-commerce. |

| Security | Ensure that imported products comply with EU standards. |

| Fairness | Reduce the unfair competitive advantage of third-country sellers. |

| Control | Better regulate the massive flow of direct imports. |

The European Commission observed that, under the previous model, a significant share of goods imported via online sales platforms did not comply with European safety requirements. By imposing this customs duty, the EU strengthens border controls while limiting distortions of competition that penalised economic operators established within the European area.

Why is this measure being introduced?

The figures speak for themselves. In 2025, European Commission statistics revealed that nearly 5.9 billion low-value items were shipped from third countries to European consumers without being subject to customs duties. This massive volume demonstrates how outdated the old system had become in the face of the massive flow of modern e-commerce.

For many foreign sellers, this regulatory framework allowed them to offer extremely low, highly competitive selling prices because these products were not subject to the same tax and regulatory pressure as goods produced or distributed by European companies. The latter, subject to strict tax, social and environmental obligations, found themselves at a competitive disadvantage.

By introducing this flat-rate €3 customs duty, the European Union is therefore acting pragmatically. The aim is to restore more balanced competitive conditions. This tax is not only a source of revenue for the customs budget; it is above all a regulatory tool designed to ensure that every player, regardless of their country of origin, contributes to the compliance and safety effort that governs the European single market.

In which cases does the flat-rate €3 customs duty apply?

Precision is essential for e-commerce companies. According to the explanatory notes published on 2 June 2026 by the European Commission, this €3 duty specifically concerns distance sales of imported goods (DSIG) whose intrinsic value does not exceed the €150 threshold.

The application of this tax is cross-cutting. It is due in the following situations:

- When the seller or platform uses the IOSS (Import One-Stop Shop) regime to declare its distance sales.

- When goods are sent by post, whether under special regimes or the standard import VAT regime.

An essential point to remember: the application of the €3 duty is independent of the customs declaration procedure. Whether the importer uses an H1 declaration, an H6 declaration or an H7 declaration, the flat-rate duty remains payable. As soon as the value and import method conditions are met, the tax must be paid. There is no way to circumvent it based on the choice of customs declaration type.

| Declaration regime | Applicability of the €3 duty |

| H1 declaration | Yes |

| H6 declaration | Yes |

| H7 declaration | Yes |

| Sales via IOSS | Yes |

What is a distance sale of imported goods (DSIG)?

It is essential for every seller to fully understand the definition of a DSIG in order to know whether their operations are subject to the tax. A distance sale of imported goods (DSIG) refers to any transaction involving goods shipped from a territory located outside the European Union to a final consumer established in an EU Member State.

The legal definition of this concept is established by Article 14, paragraph 4, point 2 of VAT Directive 2006/112/EC3. This definition is broad: it covers goods shipped or transported by the supplier itself, or on its behalf, including situations where the seller intervenes indirectly in the organisation of transport (for example via an e-commerce platform that facilitates logistics).

What are the conditions for a sale to be classified as a DSIG?

For customs authorities to classify an operation as a DSIG and thus apply the €3 customs duty, four cumulative conditions must be met:

| Condition | Details |

| Seller status | Must be a VAT taxable person. |

| Buyer status | Non-taxable person (individual) in the EU. |

| Location of goods | Goods located outside the EU at the time of sale. |

| Shipment | Transport managed or organised by the seller. |

An important clarification completes these rules: if a final customer organises the transport of their goods themselves without any direct or indirect intervention by the seller, then the operation is not classified as a DSIG. Similarly, if the sale to the consumer takes place after the goods have already been released for consumption within the EU, the flat-rate customs duty does not apply.

What is the anti-abuse clause?

The European Union anticipated attempts to circumvent this new tax. The anti-abuse clause was introduced to enable customs authorities to counter practices that would seek to avoid payment of the €3.

The mechanism is simple: in the case of complex transaction chains, customs analyse the entire process, from the origin of the goods to final delivery. The objective is to precisely identify which transaction constitutes the DSIG. The rule is clear: the clause prevents any artificial splitting of shipments or any concealment of the nature of a sale intended to evade taxation. In short, whatever the structure of the transaction, if it meets the DSIG criteria, the €3 tax is due.

How is the intrinsic value of goods per shipment determined?

The concept of “intrinsic value” is central to the application of the tax. It serves as the benchmark to determine whether a package is subject to the €3 duty or not. The definition, given by Article 1, paragraph 48 of Delegated Regulation (EU) 2015/24464, distinguishes two scenarios:

| Type of goods | Calculation method |

| Commercial | The intrinsic value corresponds to the price of the goods sold for export to the European Union. Note, transport and insurance costs are excluded from this calculation, unless they are included in the total price without being itemised on the invoice. All other taxes and charges verifiable by the customs authorities must also be included. |

| Non-commercial | The intrinsic value is defined as the price that would have been paid if these goods had been sold for export to the European Union. |

This calculation rigour is essential to ensure that the €150 threshold is applied uniformly by all Member States.

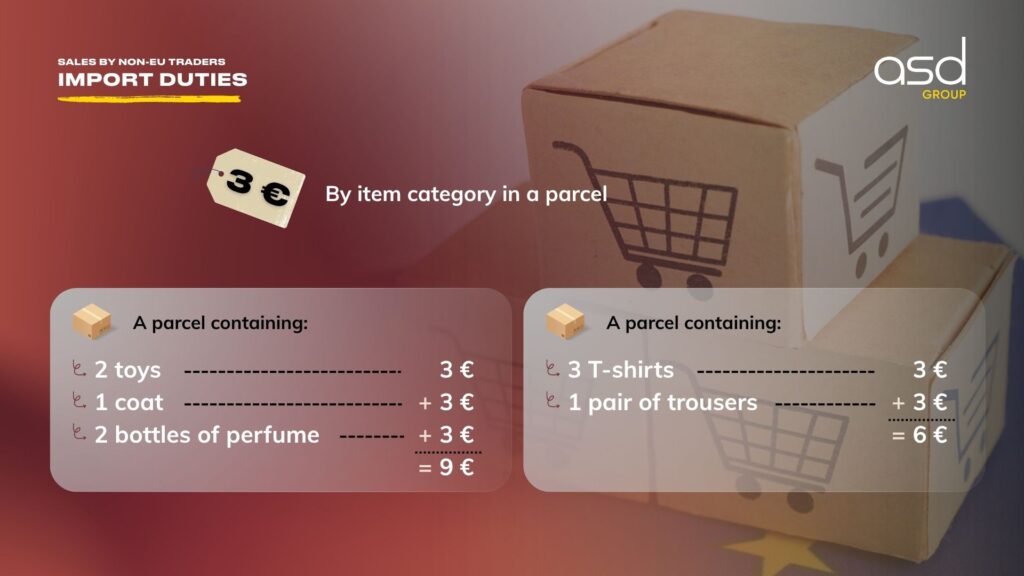

How does the flat-rate customs duty apply?

A fundamental aspect of this reform is that the €3 is not calculated “per parcel”, but “per item line”. This is a paradigm shift that requires sellers to be extremely precise in their customs declaration.

The duty applies once for each item line sharing the same customs nomenclature and, in the case of H1 declarations, the same origin. Regardless of the number of items in the line, the €3 duty is applied to the entire line.

The differences between the declarations are notable:

- H1: Requires the 10-digit TARIC code, country of origin and quantity of items.

- H6 and H7: Use the 6-digit HS CODE (8-digit NC code for H6). Origin is not required, and the quantity is not always available.

| Declaration type | Nomenclature requirement | Origin requirement |

| H7 | 6-digit HS CODE | No |

| H6 | 8-digit NC code | No |

| H1 | 10-digit TARIC code | Yes |

A major point of attention concerns the H1 declaration: it is strictly limited to a single consignee. In the case of grouped shipments, it is imperative to make a declaration per shipment. A grouped declaration for several different final consumers is prohibited in this context.

Is the flat-rate €3 customs duty included in the taxable base for import VAT?

The tax treatment of these €3 depends directly on the regime chosen by the seller.

- If the IOSS regime is not used: The flat-rate €3 customs duty must be included in the taxable base used to calculate import VAT. VAT is therefore calculated on an expanded base that includes this new tax.

- If the IOSS regime is used: The situation is different. VAT is declared and paid at the time of sale via the IOSS single window. Consequently, import VAT is not due on entry, and the €3 customs duty is not included in the VAT taxable base.

It is also important to note that this €3 duty is not eligible for any refund, even in the event of return of the goods or cancellation of the transaction after importation.

Who is liable for the flat-rate €3 customs duty?

The question of liability is decided by a hierarchy defined by the declaration method. The customs declarant is always the primary liable party for the €3 duty.

- Under the IOSS regime: The declarant is the holder of the IOSS number or their indirect customs representative.

- Under the simplified postal regime: The postal operator or its representative is liable.

- In other situations: The indirect customs representative is responsible.

- Default case: In the absence of a representative, any person able to provide the information and present the goods becomes liable.

The final consumer, for their part, is liable only in extremely limited cases, notably when the Member State concerned authorises a simplified online declaration directly for individuals.

What are the consequences for e-commerce sellers?

For B2C e-commerce players, these new rules require immediate adaptation. The increase in costs for low-value products, although flat-rate, is significant for low-margin items. It requires a complete review of pricing strategies, shipping logistics and operational models.

There are many points to watch out for:

- Customs classification and origin: The accuracy of product catalogues has become the primary lever for cost management. An error in the tariff code can lead to incorrect payment or customs detention.

- Import regime optimisation: The choice between H1 or H7 must be carefully considered according to the volume and nature of the products, as it dictates the declaration obligations and associated costs.

Faced with these changes, expert support is often the key to minimising the impact on margins and ensuring full compliance with European regulations. Do not let these new customs rules weaken your competitiveness. Customs expertise is now a strategic asset for any seller wishing to sustain their sales on the European market.

Ensure the compliance of your imports under this new regulation

ASD Group supports companies in optimising their flows and mastering new customs constraints.

Noémie Almot

Community Manager & Copywriter

Noémie is a specialised writer at ASD Group. She authors and manages blog posts and news updates across our websites, focusing on VAT, international taxes, customs operations, social regulations, and international trade. With her clear and instructive writing style, Noémie transforms complex technical and regulatory topics into accessible and practical content for businesses.